In Scaling Up, Verne says, “Growth sucks cash."

The faster a company grows, the more money you have to invest. As an entrepreneur of 18 years, I know how important it is to learn how to finance your business growth.

That’s why I want to bring you the expertise of John Mullins, associate professor of London Business School and author of “The Customer-Funded Business” to help you learn different ways to finance your business growth.

John has also built three companies, two of which were eventually sold and went on to be publicly listed. So he really understands the life cycle of taking a company from a start-up to dominating your industry.

Throughout his experience and research, he identified five different models you can use to start, finance, or grow your company with your customer’s cash instead of funding from investors.

At Growth Institute, we have used four out of five of these models to help us rapidly grow and get into the 2018 Inc. 5000 list.

I met with John to dive deep into these five customer-funded models.

Here are some highlights from that conversation along with tips you can use to correctly implement each model into your business, so you can decide which customer-funded is the best for you to fund your business growth without relying on venture capital (VC).

Should You Raise Capital To Grow Your Business?

[Daniel Marcos] Welcome John. Thank you for joining us.

[John Mullins] Thank you! So, as Daniel said, we're going to talk about how to grow your business by using your customers’ cash and without relying on investors. Let’s investigate why this is important with some opening thoughts from a guy named Bill Solomon.

Bill is a Harvard Business School professor famed as the father of the entrepreneurial finance thought world. And here's what he says about entrepreneurial finance: “The best money comes from customers; not from investors.”

Bill is a Harvard Business School professor famed as the father of the entrepreneurial finance thought world. And here's what he says about entrepreneurial finance: “The best money comes from customers; not from investors.”

Let’s take a look at some facts that support this statement.

Fact number one: The vast majority of fast-growing companies never raise external equity. I would also argue that they shouldn’t. Why? Because raising capital, whether it's from private equity guys or VC investors is actually a pretty dangerous practice.

[JM] The first drawback of raising capital is it’s a huge distraction. When you spend all your time raising capital, you’re not spending time on your customers. This leads to the second drawback, which is you’re raising money for something that you’re not certain is going to succeed, and it’s very risky.

Another drawback is you have to give away a stake in your business. This in itself comes with baggage; short-term baggage called the term sheet and longer term baggage called the shareholder's agreement. As one of my friends told me, “The term sheet giveth, the shareholder's agreement taketh away”.

I guarantee you’re not going to like the shareholder's agreement. Then, of course, there’s all the meddling you get from the investor.

So What’s The Real Cost of VC?

Let’s look at some figurative numbers.

Imagine “Entrepreneur A” wants to raise $300,000 for seed capital to fund her pre-revenue startup. She spends six months courting angels and successfully raises $250,000. Her investors get a 25% stake. Then the company is valuated to be worth a million, which means there's a pre-money valuation of $750,000.

Next, she spends six months courting customers to prove the product and the market fit together.

Another 12 months later, once the product market fit is proven, the customers start rolling in.

She then raises another round of VC with a $6 million post-money valuation and raises $2 million dollars to fund faster growth. Her investors get a 33% stake of the remaining 75%. Which leaves the entrepreneur with 50% ownership.

At a $6 million valuation, this means “Entrepreneur A” owns $3 million after 18 months of work.

Now let’s look at an alternative scenario with “Entrepreneur B”.

She spends six months focusing on her customers rather than raising capital. She successfully finds product market fit and starts selling to her customers. After another six months, her returning customers provide proof of traction.

With proof of traction, she raises $2 million at a $6 million post-money valuation, with her investors getting a 33% stake. This is the same VC deal as “Entrepreneur A”, except “Entrepreneur B” did not give way an initial 25% to angels. This means “Entrepreneur B” owns 67% of the company, worth $4 million, after 12 months of work.

[JM] Yes, in effect. And because of the dilution factor, the more rounds you raise, the more money you lose. Let’s take a look at some real-life examples: Steve Jobs vs. Michael Dell.

How Did Steve Jobs and Michael Dell Fund Their Companies' Growth?

%20(1).png?width=864&name=graphic1_dell_jobs%20(1)%20(1).png)

Steve Jobs raised many rounds of venture capital very early in the history of apple. What was the result?

Steve Jobs in the end got fired by his own investors. Yes, he did come back later to reinvent Apple and did a fantastic job, but what I’m pointing out here is you can lose so much stake in your company that your investors can fire you.

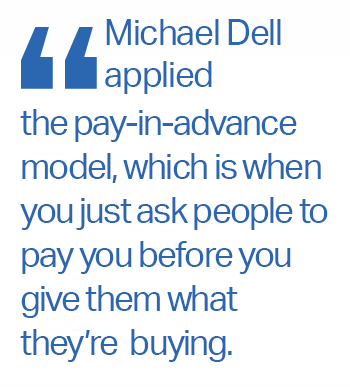

Michael Dell on the other hand got his funding from his customers as a 19-year-old college student in Texas. His customers would pay him in advance for the computer before they were even built.

Now, who do you think kept more value that was created in their company over time? Was it Dell, or Jobs?

It was Dell, hands down.

[DM] Yes, of course. Now, I’d like to highlight something you said, and that is Michael Dell used the pay-in-advance model. This is one of the five customer-funded models. What are the other four?

What Are The Types of Customer-Funded Models?

[JM] Michael Dell applied the pay-in-advance model, which is when you just ask people to pay you before you give them what they're buying.

[JM] Michael Dell applied the pay-in-advance model, which is when you just ask people to pay you before you give them what they're buying.

Another customer-funded model is the scarcity model, where you make less of something over a lesser period of time to encourage the customer to buy it right now. Next, is the service-to-product model. This is when service businesses adapt their services into a product they can sell to scale much faster.

There’s also the matchmaker model, which brings together buyers and sellers without ever touching what is bought or sold, and without having to own the assets transacted.

This brings us to the last one, which is the subscription model. Customers subscribe to a product and service for a fixed period of time, which guarantees recurring revenue the company can use to grow very fast.

What Are Some Examples of Customer-Funded Models?

[JM] Companies like eBay, Expedia, Uber, and Airbnb use the matchmaker model.

Netflix is an example of the subscription model. The world-class champion in scarcity is Zara. They limit the amount and time each style is available, so their customers know to buy that Zara dress they like now or it will be gone tomorrow.

Zara turns its inventory every 30 days but only pays its suppliers every 60 days, giving them 30 days of supply money to grow their business.

%20(1).png?width=864&name=graphic2_logos%20(1)%20(1).png)

Now, let’s look at how Bill Gates and Paul Allen used the service-to-product model to build Microsoft. Gates and Allen were in the service business. They were programmers who wrote operating systems for the new PC makers. They were profitable, but not very scalable because their time was exchanged for money.

After a while Gates and Allen decided to just create one operating system and package it as a product that can be sold again and again to different PC manufacturers. The result? MS-DOS. That's when the value of Microsoft really took off.

I’d like to know share with you my experience at GAP.

When I served as Vice President at Gap, we had only a hundred stores, mostly in California. Gap needed to scale really fast because it was in a footrace with another retailer for all the best shopping mall locations.

There were a few things we did at Gap to scale, but I want to focus on the customer-funded part. We realized there are three peak seasons in apparel: Easter, back-to-school, and Christmas. We strategized to only open our new stores right at the beginning of those three peak seasons, and not any other time of year. We also convinced our new landlords to fund the store’s renovations, such as air conditioning, floor and paint, which they agreed to do in return for a little more rent.

There were a few things we did at Gap to scale, but I want to focus on the customer-funded part. We realized there are three peak seasons in apparel: Easter, back-to-school, and Christmas. We strategized to only open our new stores right at the beginning of those three peak seasons, and not any other time of year. We also convinced our new landlords to fund the store’s renovations, such as air conditioning, floor and paint, which they agreed to do in return for a little more rent.

This meant we wouldn't have much investment in the new store except for the inventory. We managed to negotiate a 90-day term with our vendors, giving us 90 days during peak season to do a ton of business. Using the scarcity model is what enabled Gap to scale up so fast in the 1970s and become the global phenomena it is today.

The next story I want to share is from Mexico. In 1996, Simon Cohen realized that the shipping industry service was problematic in Mexico. To solve the problem, he built a business called Henco Global based on the matchmaking model that brought together people, typically retailers, who needed to ship something to Mexico.

Simon never raised a single peso of capital to fund the growth of this business, but the customers’ payments funded continual growth until today. It’s now a hundred million dollar shipping business, yet Henco Global doesn't own any trucks or ships!

Here’s another cool story, and this is one is a subscription model used by a company in India. Krishnan Ganesh built a fantastic business called TutorVista in 2005. He hired three Indian teachers to tutor kids in the US via the internet. At first, Ganesh was charging $20/hour. Business was growing, but slowly.

So Ganesh decided to try out the subscription model. For $100 a month, the kids could get “unlimited tutoring” whenever he or she needed it. Both parents and the kids loved the idea and that’s when business took off. Based on that customer traction, Ganesh successfully raised $2 million from Sequoia Capital, and later raised another $10 million.

Later, he sold the business to Pearson for north of $200 million!

So How Do You Know Which Model Is The Best One To Use For Your Business?

[JM] Here are some questions you could ask yourself to start identifying which model could work for you:

For pay-in-advance model:

- What could you get your customers to pay you in advance for?

- Why might it be in my customer’s interest to pay me sooner?

- What is the additional value your customers get by paying in advance?

- Can your offer be limited in time or quantity to create an exciting scarcity?

- Why might your supplier be willing to give you longer terms?

- Could you get your customers to subscribe instead of reordering from you?

- Is there something in your product mix which customers are willing to get by subscription that just shows up every month, like with the Dollar Shave Club or like how Adobe switched to a subscription so customers will always have the latest version?

- Do you see a problem you can solve by playing the role of a matchmaker that brings together buyers and sellers?

- Are your buyers and sellers fragmented in the market?

- What service, which you provide over and over again, could you kind of put in a bottle or a box, just like how Microsoft did to scale?

What's The Best Way To Implement These Models After Identifying Is Best For Your Business?

So now I'd like to take the wheel.

Let's get into how to implement these models into your business.

First, I strongly recommend getting John’s book. We bought a few copies of John’s book for our management team. And as I mentioned earlier, Growth Institute then applied four out of five of these models to help us rapidly scale.

Second, you have two options inside London Business School where John teaches as an associate professor.

The first option is their Executive MBA, which costs around $110,000. They also offer 2-3 day executive education programs which cost around $9,000. These are all great options and if you can pay for them, it’s very strongly recommended.

- You’ll participate in an interactive, online certification program, spread over 9 weeks.

- You’ll get a new video training every week (more than 9 hours of study material).

- You’ll go through 9 highly interactive live, online workshops directly with John, including the chance to pose your burning questions.

- You’ll join your peers in 5 facilitated in-depth masterminds where you will delve into the application of course in smaller more intimate groups.

- We’ll lead you through interviews and insights from some of the world’s top executives who used the five customer-funded models to scale their companies.

- All the video recordings and extra materials are yours to keep for 12 months from the start of the program.

You’ll also get activities and assignments to implement in your business. We believe that learning without implementation goes to waste so we want to make sure we give you all the tools you need really understand how to implement these models in your business and get results.

John is really the best person you can learn from when it comes to scaling your business without VC. He’s an entrepreneur at heart, and he's also a professor so he understands how to teach this and how to walk you through the process, so you can implement it in your business.

-(1)-small%20(1).png)